Content

Unlike job order costing and process costing systems, activity based costing systems only assign costs to products that are related to manufacturing activities. In addition, nonmanufacturing costs that are related to manufacturing activities, such as customer support costs and selling costs, are assigned to products in an activity based costing system. Many small-business owners believe that this type of costing system allows them to make more sound decisions, because more relevant costs are accounted for and nonrelevant costs are not. Standard costing is an accounting system where you establish standard rates for materials or labor used in production or inventory costing. By doing this, you can work out the labor and material costs to produce a single unit of your product. Manufacturing cost accounting encompasses areas that impact production operations and the valuation of inventory. These activities can significantly boost the profits of a business, as well as bring it into compliance with the applicable accounting standards.

John Freedman’s articles specialize in management and financial responsibility. He is a certified public accountant, graduated summa cum laude with a Bachelor of Arts in business administration and has been writing since 1998. His career includes public company auditing and work with the campus recruiting team for his alma mater. In order to ensure that the accounting process of the manufacturing firm goes along well, the expenses should be properly noted. This can help the higher management to study the trends and plan strategies which can help in reducing the expenses.

The rules made sense a century ago, when the world was very different, but today these old rules incentivize the wrong behaviors. But as Locher explained, as inventory turns increase, the time between “money out” and “money in” decreases, so matching becomes less of an issue. Provide at least three additional detailed pieces of financial information that would help managers evaluate performance at UPS. Provide at least three additional detailed pieces of financial information that would help managers evaluate performance at Home Depot. Match each previous item with the most accurate description as follows. Provide at least three additional detailed pieces of financial information that would help managers evaluate performance at Ford.

Factors That Influence Adoption Of Management Accounting Technique

Improved productivity by freeing your employees to work on core business areas. Finished inventory can lose value when in storage awaiting shipping to a client. The manufacturer must review inventory and update the value of the product on the balance sheet to reflect such loss of value/obsolescence. People respond by making changes that may lead to increased costs and lower revenues . In these cases, Locher said, large manufacturers could learn something from the small, build-to-order job shops. When the orders aren’t there, they stop producing, they don’t consume material, and they plug the cash drain. They may end up having to lay off people eventually, but it’s an act of last resort.

The key is to maintain that commonsense simplicity as the accounting department grows. Locher clarified that “budgeting” differs from a financial analysis to determine future needs, such as for capital spending like equipment and plant expansions, as well as hiring. “That’s looking at cash, what’s coming in and what’s going out. To figure this, now you divide $10 million by 150,000, and you get an overhead rate per hour of $66.67. That improved job is now, to use some financial parlance, underabsorbed.

They are the lowest organizational level within your business and the level at which you account for all revenues, expenses, assets, liabilities, and equity. To determine a company’s net worth, you must review the results at the end of the previous fiscal period and then take into account changes that have occurred during the year. Hiring outsourcing accounting servicescan prove to be extremely advantageous as they are capable of managing complex data. This can also eliminate the need for having in-house accounting staff and offering them infrastructure. The following T‐accounts illustrate the impact of the closing entries on the special closing accounts and retained earnings.

When products are in the production line, the total cost up to the point of their progress must be known and included in the manufacturing account. Standardization of the production costs makes tracking easier. Joyce Warnacut’s book, The Monetary Value of Time, describes how absorption costing penalizes improvement practices. So you divide $10 million by 200,000, and you get an overhead rate of $50 an hour. Now let’s say you improve a process, increase part flow velocity, and produce the same job in 150,000 hours. This frees capacity and sets the foundation for the operation to be profitable and flush with cash. This made perfect sense financially in the days when direct labor cost nearly two-thirds of annual revenue.

Variances occur when the frozen standard costs differ from other user defined cost methods, such as current costs. These variances can be due to differences in labor or overhead, or changes to the bill of material or routing. The chart of accounts is a record of the valid accounts you assign to the business units within your company’s reporting structure. When you set up your chart of accounts, you define the location of the accounts using automatic accounting instructions that indicate which number ranges represent assets, liabilities, and so on. First, the business makes a record of each transaction — whether purchase, sale, loan or repayment — when it takes place. Second, the business totals these transactions into ledger accounts. Each of these accounts covers a specific category of activity such as revenue, expenses, accounts payable, accounts receivable, cash on hand or capital.

What Is Manufacturing Cost Accounting?

In fact, many of them began working with us in the beginning years of their business and remain with Accounting Freedom today. We also implement a periodic inventory system or perpetual inventory system to track the number of products on hand at any time in your production line. Our perpetual inventory gives accurate inventory unit quantities at all times. In the competitive manufacturing industry, it is imperative to follow the best accounting principles to run a profitable operation. This not only helps with compliance but also makes your business more competitive. Our accounting firm has been around since 2007 but our accountants and researchers have decades of combined experience. It is this experience we bring onboard your manufacturing business coupled with extensive resources and flexibility in accounting solutions.

At the end of the company’s fiscal year, the physical inventory count showed $9,000,000 less than Rite Aid’s inventory balance on the books, presumably due to physical deterioration of the goods or theft. Rite Aid executives allegedly failed to record this shrinkage, thereby overstating ending inventory on the balance sheet and understating cost of goods sold on the income statement. Manufacturing businesses have to account for their raw materials and processing costs, but they also have to work out the value of the finished items they create. This will be an accumulation of the money you have spent on direct materials, direct labor costs, and manufacturing overheads on each work-in-process item in your inventory.

The more ending inventory you have, the less your COGS, and the greater your profit. It’s one reason that financial people resist lean, which initially reduces “ending inventory” and, hence, increases the COGS and decreases profits, at least on paper. A soft close gives a quick view of profit and losses as well as cash flow—what money was spent and what money came in during a specific period—again, as recent as possible. If a customer hasn’t paid yet for a shipped job, that’s fine; it can be accounted for at the next close, be it a day or week later. Review Note 1.48 “Business in Action 1.6” Provide two examples of selling costs and two examples of general and administrative costs at PepsiCo. Explain why ethical behavior is so important for finance and accounting personnel.

Prepare a schedule of cost of goods manufactured for the month of March. Indicate whether each item should be categorized as a product or period cost. Maria is the loan officer at a local bank that lends money to Old Town Market, a small grocery store. She requests several quarterly financial reports on an ongoing basis to assess the store’s ability to repay the loan. Provide one example of a financial accounting report and two examples of managerial accounting reports that Maria might request. Describe the inventory cost flow equation and how it applies to the three schedules shown in Figure 1.7 “Income Statement Schedules for Custom Furniture Company”. Describe manufacturing costs and nonmanufacturing costs.

This can also be tied to activities such as customer service. Time-driven activity-based costing is a variation of this, which accounts for costs over a given period. Your manufacturing accounting software should also help you keep compliant with regulations and the tax laws of the countries you have a business in. Often, manufacturers invest in an all-in-one solution, which handles other tasks away from finances, such as planning and production. Ideally, data should move freely between production lines and the back office, meaning you have accurate real-time data. Many manufacturers use the ‘first-in, first-out ’ method, where products are sold in the order they are added to inventory. A popular way of costing inventory; this could work for businesses that have products with a shelf life.

Nanofiber Company Big

A layoff would reduce the payroll burden and free up cash, and the company could remain a going concern. Today, unfortunately, when times get tough, too many companies do what corporations did 100 years ago.

We work closely with you to account for all expenses your company incurs while making products for resale. But because inventory (i.e., the materials you need to manufacture your product) requires cash, it can be seen as a liability for some. How you handle this in your books and in practice can make a huge difference to your bottom line. Depending on what you’re making, you may spend months sourcing raw materials. Rather than just buying the item you’re selling from a wholesaler, you have to make it, first building your assembly line or another manufacturing method, and then actually producing the item.

In addition to the regular business unit.object.subsidiary method of account coding, you can use subledger accounting. Subledgers are “subdivisions” of account details for categories that you do not want in the permanent chart of accounts.

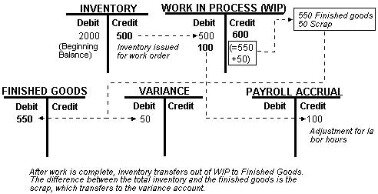

It also helps you to manage the costs by providing information to the company’s business plan. The second is to change the Frozen Standard Cost of a parent or component in the F30026 when there is a work order in process. When there are existing costs and they get changed in the middle of producing an item, this leaves a balance in WIP when P Completions is run. You can revalue WIP when there is a change to Frozen Standard Costs by setting the processing options in Frozen Update .

That is, the company records how many hours of labor and how many units of materials are used to make the product, multiplies these figures by the cost per unit and tracks the cost by job. Overhead costs, those costs that cannot be easily traced to individual products, are then allocated to products. At the end of an accounting period, at the end of the financial year, you will want to have a value associated with the number of goods in your inventory. Valuing your inventory will help establish the costs of goods sold and how much profit you are making. Having a shortage or excess inventory directly affects the production and profitability of your manufacturing business. The goal of going through the process shown in Figure 1.7 “Income Statement Schedules for Custom Furniture Company” is to arrive at a cost of goods sold amount, which is presented on the income statement.

- These activities can significantly boost the profits of a business, as well as bring it into compliance with the applicable accounting standards.

- Along with direct materials and direct labor, you must include the cost of manufacturing overhead to ensure you get the right valuation when it comes to inventory and selling price.

- The methods of analysis above will help you refine your budgets for the next accounting period, though you’ll need to take into account more detailed production schedule information too.

- Since then, many other industries have come to regard removing waste from their processes as beneficial to the bottom line.

- They calculated the cash spent for material, machine operators, supervisors, and extra facility costs, like electricity consumption, during the second shift.

- For example, an orange juice manufacturer, a gravel mine and a maple syrup bottler would all be likely to use process costing.

Two college graduates recently started a Web page design firm. The first month was just completed, and the owners are in the process of comparing budgeted revenues and expenses with actual revenues and expenses for the month. Would this be considered part of the planning function or the control function?

Myth No 3: Inventory Is An Asset

For instance, a company not meeting the budget may put a capital equipment purchase on hold. That new machine would reduce costs (e.g., one operator produces more in less time) and free capacity that could be filled with more sales. And even if those increased sales don’t come to fruition, the company would still be spending less on labor than it otherwise would have. They calculated the cash spent for material, machine operators, supervisors, and extra facility costs, like electricity consumption, during the second shift. After adding it all up, they found that it was less than what they were paying to outsource the job.